אִם יִרְצֶה הַשֵּׁם

Why one should care about SRT

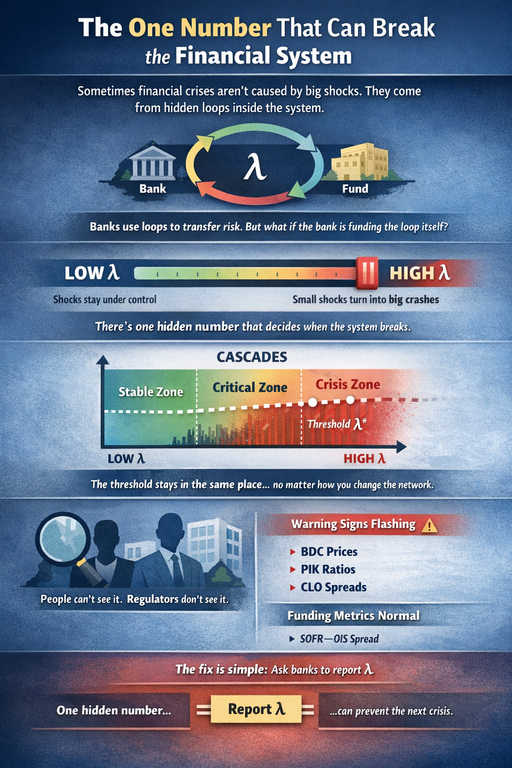

Most people think financial crises come from big shocks. A war, a rate spike, a housing bubble. The truth is quieter. Sometimes the system breaks because of a small loop that grows in the dark.

Right now that loop sits inside a part of the credit market called synthetic risk transfer. Banks use it to move credit risk to outside investors. On paper this looks simple. A bank pays a fund to take the hit if loans go bad. The bank gets relief on its capital rules. The fund gets a steady stream of payments. Everyone is happy.

The trouble starts when the bank is also the one who funds the investor. That creates a circle. The bank pays the investor, the investor uses the bank’s money to protect the bank, and the loop tightens. Your paper shows that this loop has a single control knob. Call it lambda. It measures how much of the protection is secretly financed by the bank itself.

When lambda is low, the system behaves like the textbooks say it should. A shock hits, losses move around, and the system settles. As lambda rises, the loop begins to matter. At a certain point the system flips. Small shocks turn into large cascades. These cascades are not caused by bad loans or panicked markets. They are created by the loop itself.

The surprising part is how stable the threshold is. Change the size of the network, the number of investors, the size of the shock, or the thickness of the tranches. The critical point barely moves. It sits near the same value of lambda every time. That makes it a real physical feature of the system, not a quirk of a model.

The public never sees lambda. Regulators do not see it either. Banks know it, but they do not report it. So the system can drift toward the critical point without anyone noticing. You can see hints of this drift in market data. Prices of business‑development companies, payment‑in‑kind ratios, and spreads on certain credit products all show stress. The usual funding indicators show nothing.

This is the kind of blind spot that has caused trouble before. A small structural feature grows until it becomes the whole story. The fix here is simple. Ask banks to report lambda. Set a safe upper bound. Keep the loop from tightening past the point where the system becomes unstable.

The public does not need to know the math. They only need to know that a single hidden number can decide whether a shock stays small or becomes a crisis. And that number is easy to measure once you ask for it.

Regulator‑facing

The paper explains why lambda should be added to the standard set of Pillar 3 disclosures. Lambda is the share of synthetic credit protection that is effectively financed by the originating bank. It is a structural parameter. It is not a model assumption.

The key result from the paper is simple. In network simulations of bank‑to‑NBFI synthetic risk transfer, lambda controls a phase change in system behavior. When lambda is below roughly 0.85, shocks propagate in a normal way. When lambda enters the 0.85 to 0.95 range, cascades begin to grow faster than expected. When lambda reaches about 0.95, the system produces Dragon King events. These are outsized cascades created by the feedback loop itself.

This threshold is stable across changes in network density, investor concentration, shock size, and tranche thickness. Only the scale of the cascades changes. The location of the threshold does not. This makes lambda suitable as a supervisory metric. It is invariant across model choices and market configurations.

Banks already know their own lambda values. They compute them internally when structuring SRT deals. Regulators do not see these values. Current disclosures do not reveal them. As a result, supervisors cannot place the real system on the phase diagram. They cannot tell whether the system is in the safe region or near the critical point.

Market proxies give partial signals. Six indicators were tested. Four show stress as of early 2026. The standard funding stress measure, SOFR minus OIS, shows none. This mismatch suggests that the loop is tightening while the usual macro indicators remain calm.

The recommended policy action is minimal. Require banks to disclose lambda. Set a conservative upper bound of 0.30. This keeps the system far from the critical region. It does not require new capital rules, new reporting frameworks, or bans on SRT. It only requires transparency on a number banks already compute.

Lambda is a clean supervisory tool. It is measurable, stable, and tied to a real structural feature of the system. Adding it to Pillar 3 closes a blind spot at low cost.